Total Project Base Capital Expenditure

Rail Construction Jobs (50% in NT)

Permanent Operations & Maintenance Rail Jobs

Rail & Rolling Stock

PIB Steel Complex Industrial Land Sites (WA & QLD)

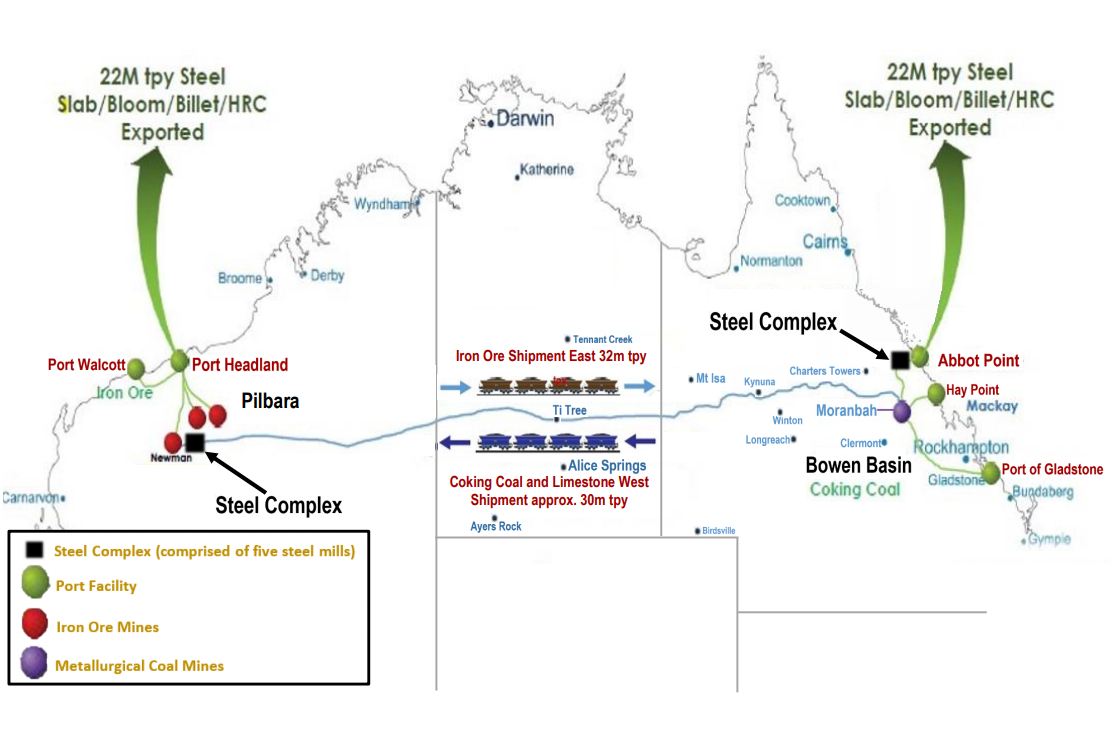

10 Steel Plants (5 on each end – owned and operated by the steel mills)

Before the 2nd world war and over 2,000 years before that, iron and steel was made next to the mines. The PIB case is a return to that best practice and correcting this modern age inefficiency and phenomena of the world’s biggest bulk ships and trains returning empty half the distance. Putting and end to the empty load phenomenon will save net billions per year. The av IO fe 60% the rest is dirt 40% – empty return trip ship and train efficiency is therefore around 30%.